The complexity of Medicare and the myriad options enrollees face can be daunting. Here are some pointers on how to go about enrolling for Medicare, and suggestions on different alternatives such as working with a Medicare advisor.

As any American over 65 knows, signing up for Medicare is not simple. There are four different parts, each with different options that can have widely divergent effects on costs and coverage. Enrollees may also wish to supplement their Medicare with private coverage. If you are approaching that landmark birthday, consider the following pointers to guide you through the enrollment process.

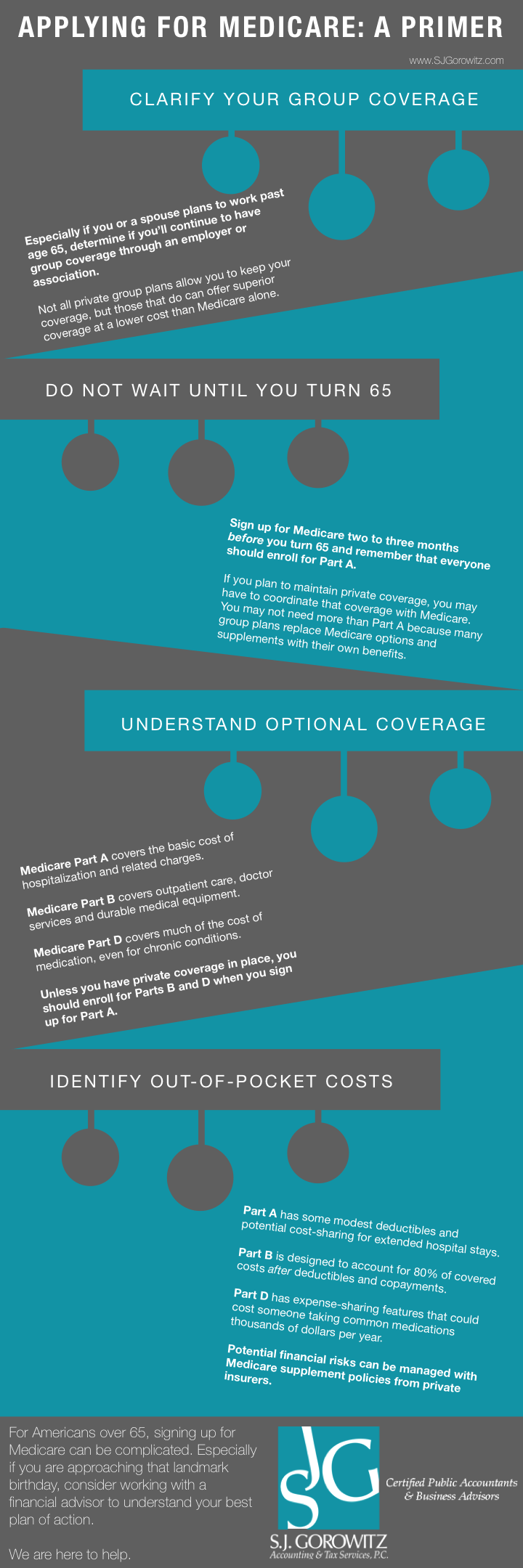

Start by determining whether you’ll continue to have group coverage through an employer or association. This is an especially important first step for anyone who continues to work past age 65 or who can be covered by a spouse who continues to work. While not all private group plans allow people to keep their coverage after age 65, those that do could help give you better coverage at a lower cost than Medicare could alone, even after all of Medicare’s options are factored in. (Keep in mind that a purely Medicare-based strategy may still be a better deal in some circumstances).

Start by determining whether you’ll continue to have group coverage through an employer or association. This is an especially important first step for anyone who continues to work past age 65 or who can be covered by a spouse who continues to work. While not all private group plans allow people to keep their coverage after age 65, those that do could help give you better coverage at a lower cost than Medicare could alone, even after all of Medicare’s options are factored in. (Keep in mind that a purely Medicare-based strategy may still be a better deal in some circumstances).

Sign up for Medicare two to three months before you turn 65 to minimize the risks of a gap in coverage. Everyone should enroll for Part A; it has no premiums for anyone who has paid Medicare taxes or was married to someone who did. If you plan to maintain private coverage, you’re likely to be asked to coordinate that coverage with Medicare. What’s more, you may not have to proceed any further in this process since many group plans replace the welter of Medicare options and supplements with their own benefits.

Evaluate Medicare’s optional coverages. Part A is coverage for the basic cost of hospitalization–things such as a semi-private room for treatment and rehabilitation, along with related equipment and service charges incurred while in the institution. Other potential costs are addressed by optional coverages. Medicare Part B covers a major portion of costs for outpatient care, doctor’s services and durable medical equipment. The base cost for this coverage is $104.90 per month in 2015, increasing for individuals whose annual income was more than $85,000 in the prior year. Medicare Part D covers a significant portion of the cost of medication, even for chronic conditions. Part D terms and costs vary widely, so consider each one in the light of your medications and other needs. Note that unless you have private coverage in place, you should enroll for Parts B and D when you sign up for Part A. If your private coverage is later cancelled, you can readily switch over to Medicare. But if you merely forego coverage now, you’ll be limited to open enrollment periods if you desire coverage later. You’ll also face late enrollment penalties and higher premiums.

Prepare for out-of-pocket expenses. Part A has some modest deductibles and potential cost-sharing for extended hospital stays. Part B is designed to account for 80% of its covered costs after deductibles and copayments. Part D has a variety of expense-sharing features that could cost someone taking common medications thousands of dollars per year. These potential financial risks can be managed with Medicare supplement policies from private insurers. Premiums may vary widely based on terms and conditions.

One final wrinkle is Medicare Advantage, a managed-care alternative to traditional health coverage under Parts A and B. The exact terms of this coverage vary and are set by the insurance companies that offer these plans. As with the other private insurance choices, there may be complex tradeoffs.

Mike Rothfarb, CIMC; Senior Vice President Wealth Management

Morgan Stanley Alpharetta / 770-643-7633

Article by Wealth Management Systems Inc. and provided courtesy of Morgan Stanley Financial Advisor.

The author(s) are not employees of Morgan Stanley Smith Barney LLC (“Morgan Stanley”). The opinions expressed by the authors are solely their own and do not necessarily reflect those of Morgan Stanley. The information and data in the article or publication has been obtained from sources outside of Morgan Stanley and Morgan Stanley makes no representations or guarantees as to the accuracy or completeness of information or data from sources outside of Morgan Stanley. Neither the information provided nor any opinion expressed constitutes a solicitation by Morgan Stanley with respect to the purchase or sale of any security, investment, strategy or product that may be mentioned.

© 2014 Morgan Stanley Smith Barney LLC. Member SIPC.

CRC 1051952 [11/14]

Source: The Official U.S. Government Site for Medicare [http://medicare.gov/]